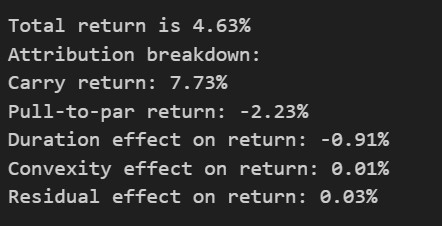

It is common for fixed income holders to want to understand what contributes to their fixed income securities return. Hence, this project develops a framework to break down the return from the fixed income securities. Specifically, it is broken down as follows:

- Carry: this is the yield earned fixing the yield curve

- Pull-to-par: this is the market value movement as the portfolio slide down the yield curve

- Duration: this is the pnl from parallel interest rate/z-spread movement

- Convexity: this is the second order impact from the parallel interest rate/z-spread movement

- Residual: as the duration moves continuously with interest rate, the duration-convexity calculation is only an approximation, and there will be high order residuals. The residuals are expected to be small if the interest rate movement is small.

BZ Consulting has developed an automated tool based on python to finish the above-mentioned attribution for large portfolios with ease. If you are interested, feel free to call/email to discuss!